Cashback Checking

Focus Groups & Product Strategy

Credit cards are the first choice for daily spending. People just don’t really use debit cards anymore. And for good reason - you can’t beat the points! A local credit union wanted to experiment was something different. They were considering rolling out a new product line that would challenge the status quo: checking accounts with cashback rewards. To ensure their vision aligned with consumer needs, I stepped in to curate and analyze two rounds of focus groups that would inform product strategy.

Team

Drew Hopkins (Me) - UX Designer and Researcher

Tracey Dunlap - Senior Creative Director

Tools

Illustrator, Lookback

Tactics

Survey/screeners, prototypes, focus groups

Strategy

After consulting with the credit union, Tracy (Senior Creative Director) and I determined our primary research goals together:

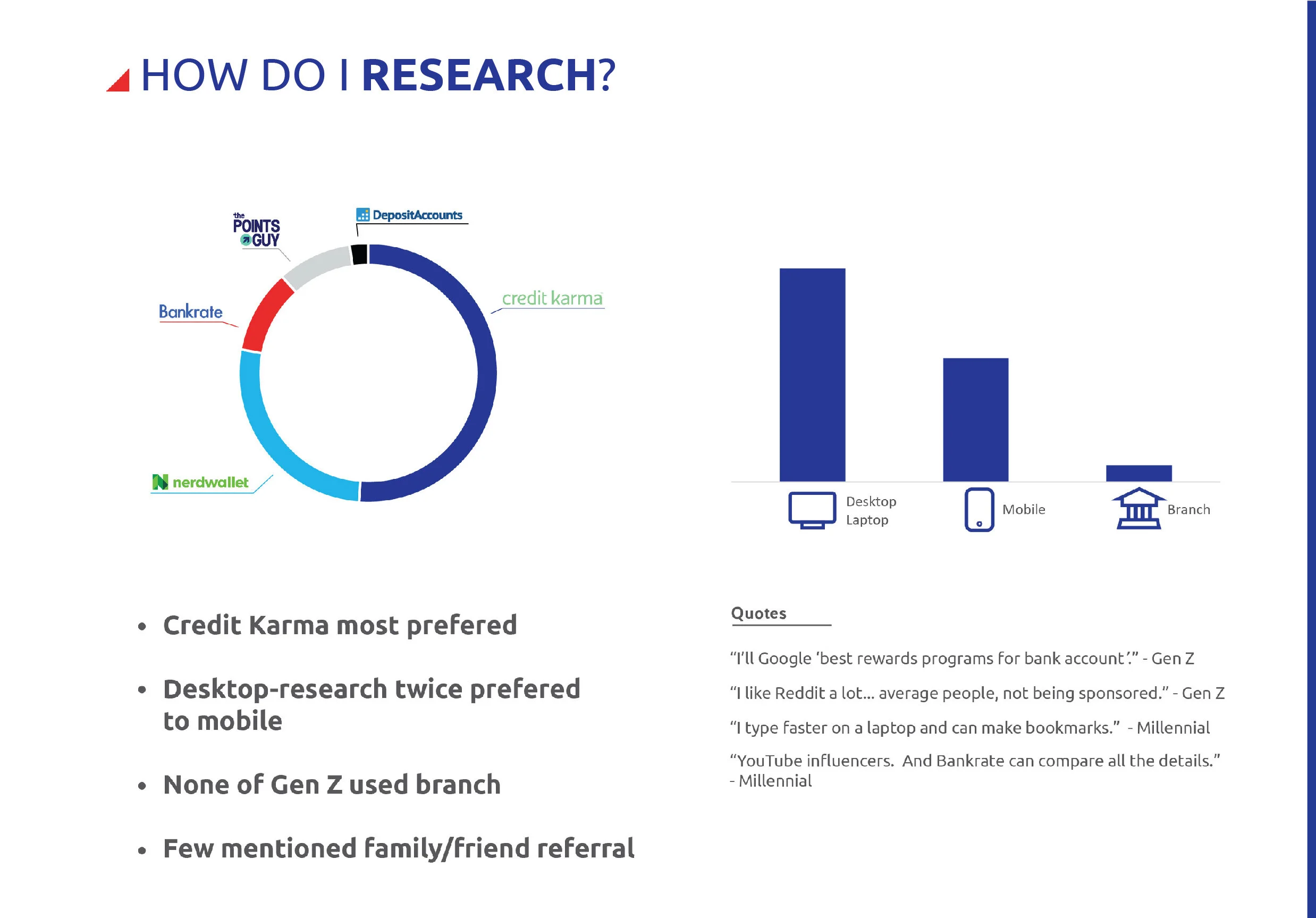

How do consumers research and choose their financial institutions?

What pain points due they have? Why would they switch banks?

What are consumers perspectives on checking accounts?

What causes distinction or choice in day-to-day cash management?

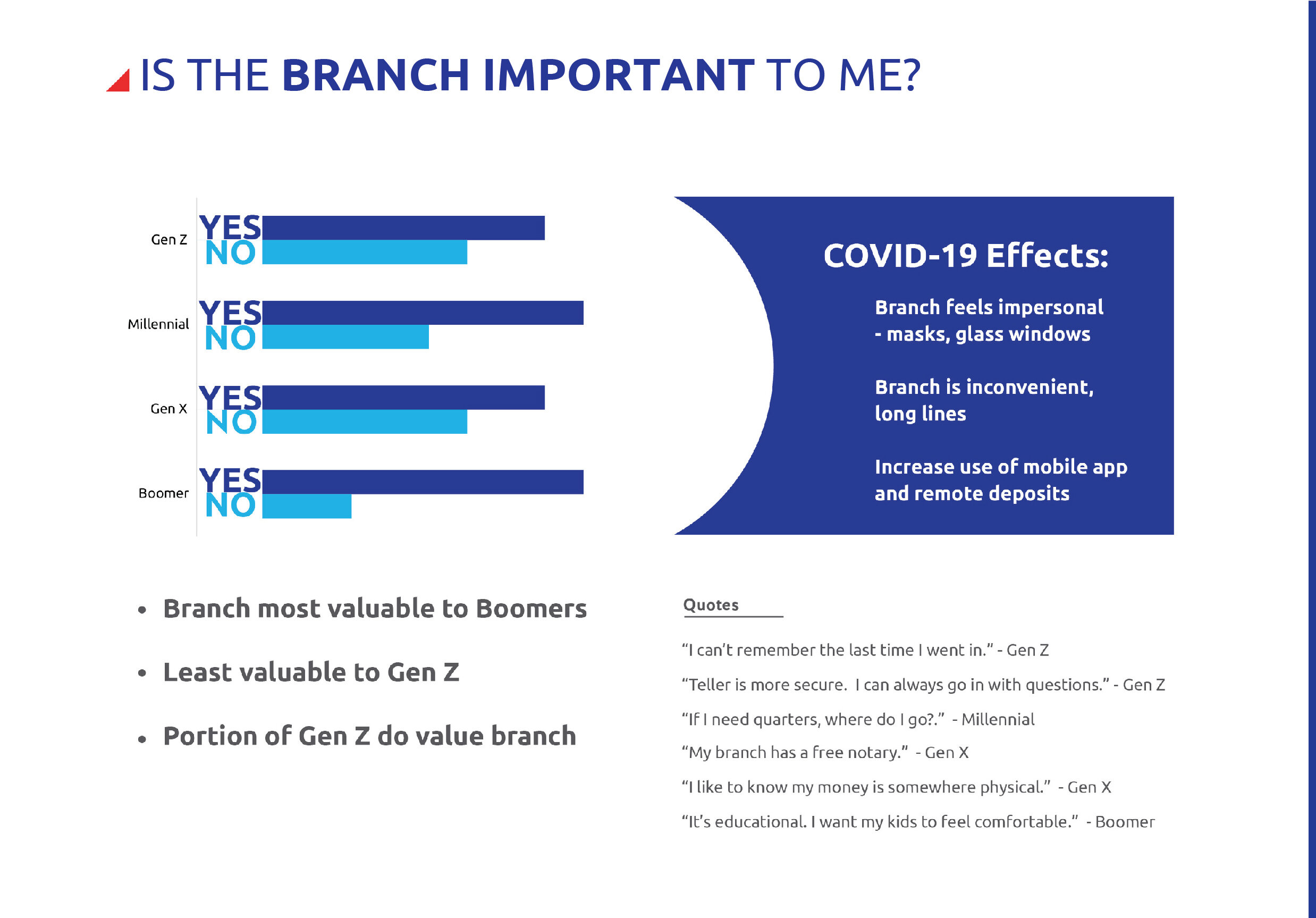

Does the branch matter? Do ATMs?

Do the offers and product designs resonate?

How are the products better than the competition? Weaker?

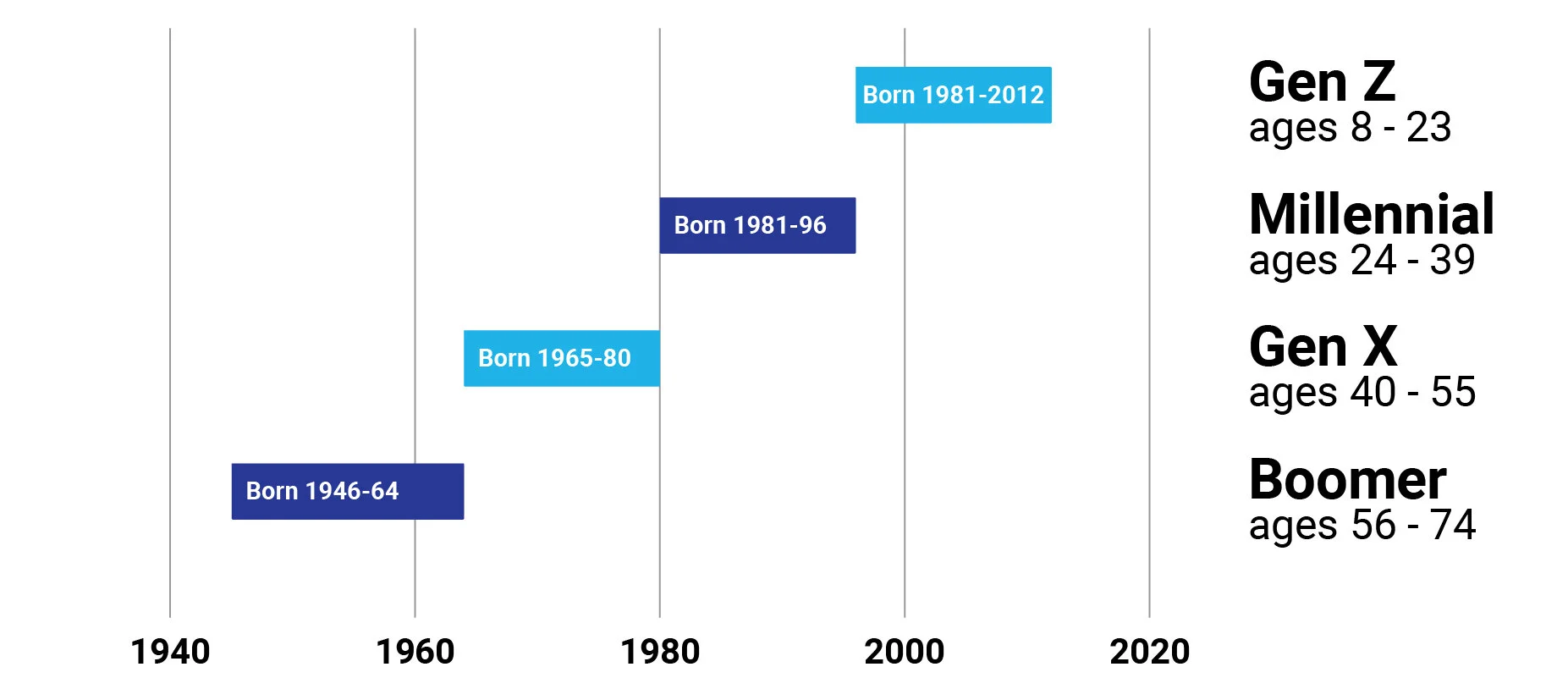

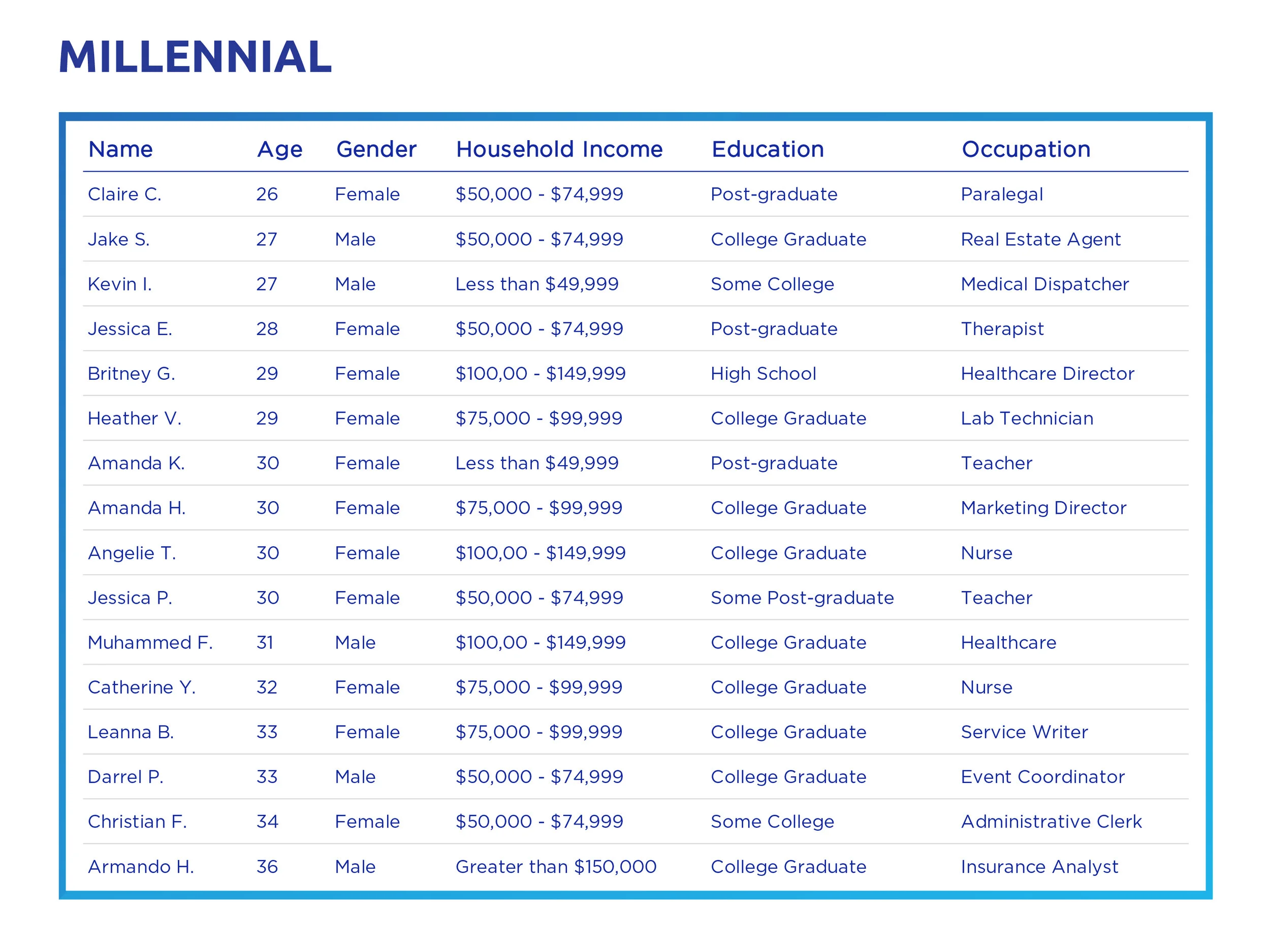

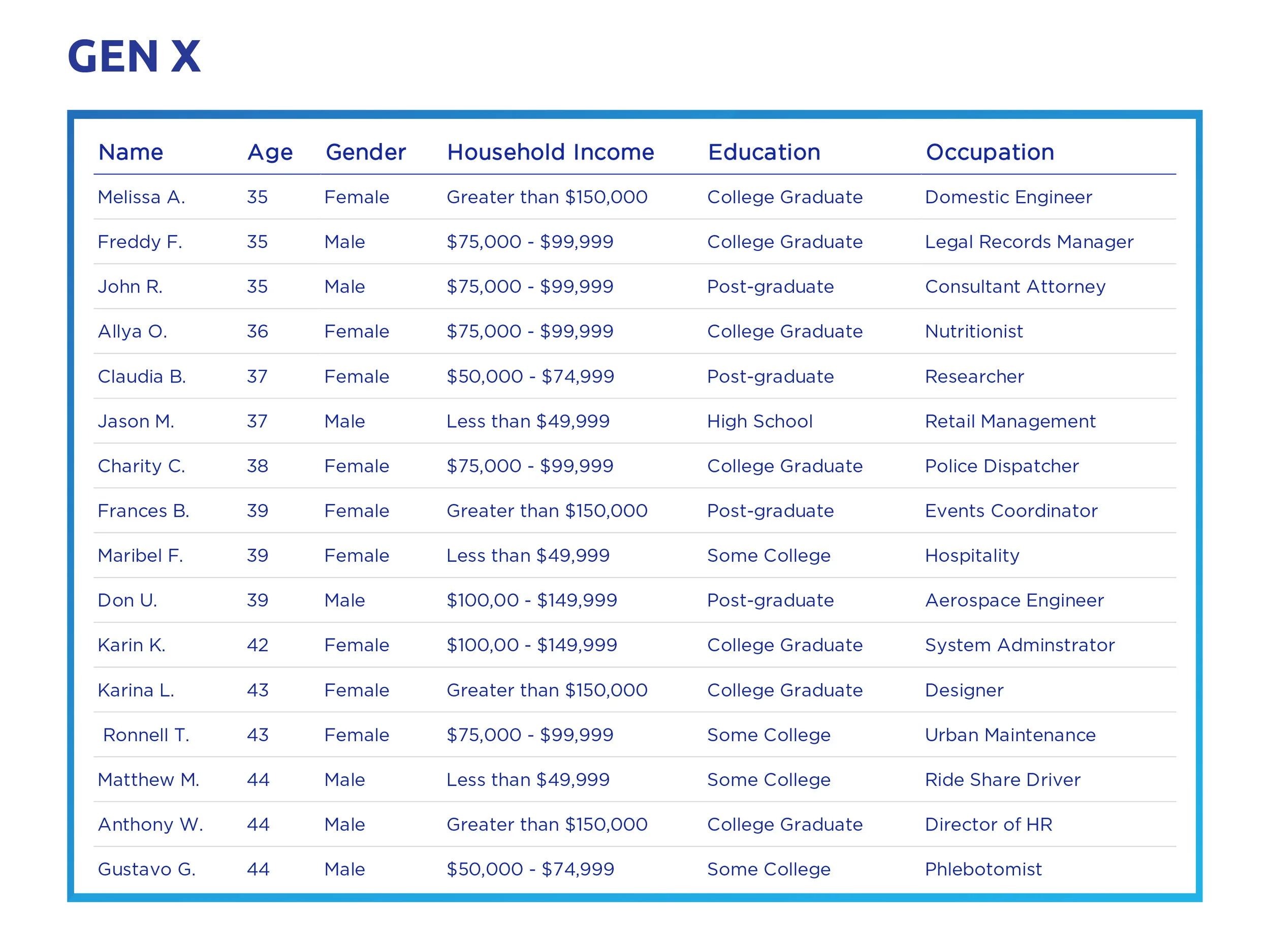

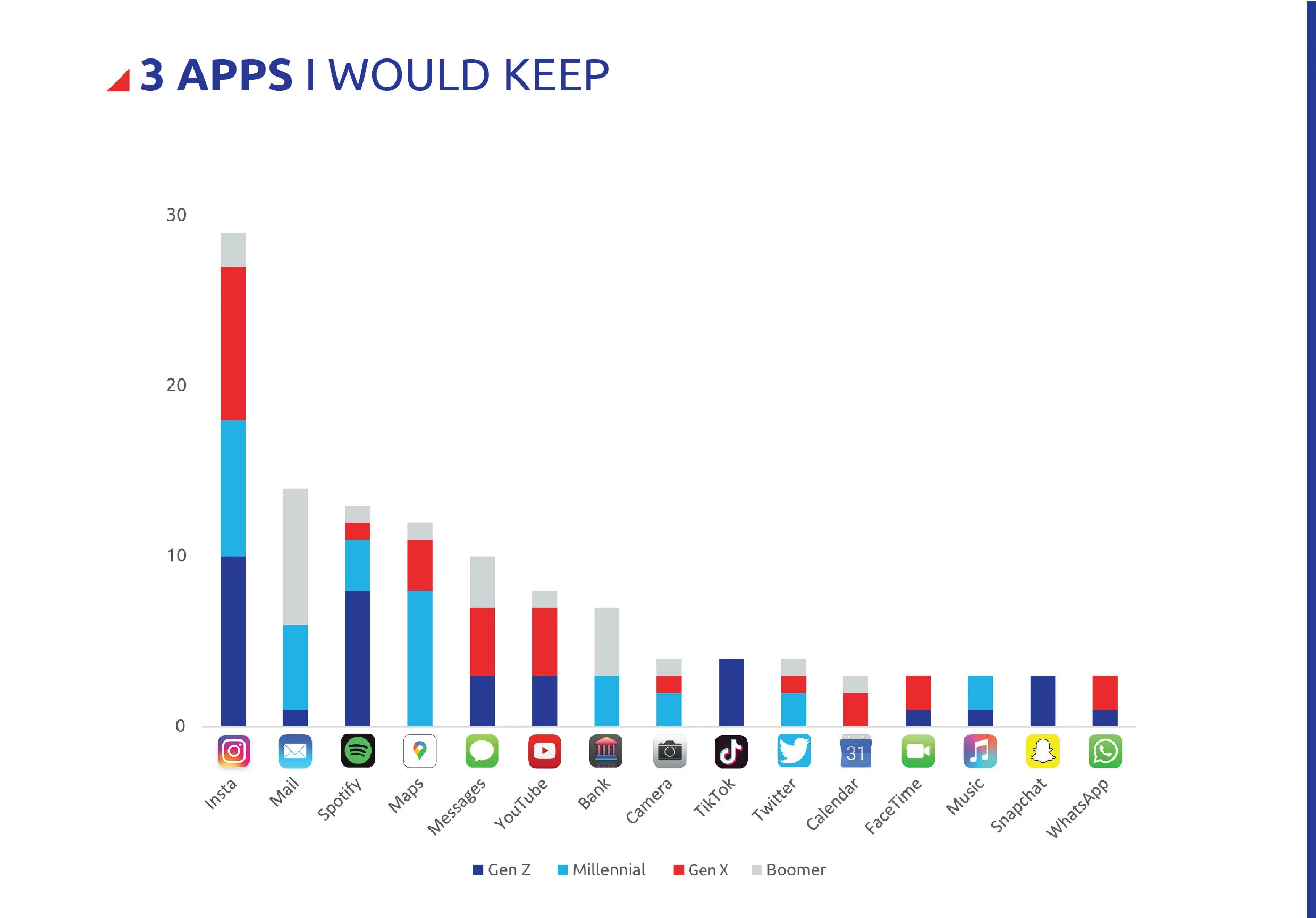

In previous research studies, we found that age was the variable that most drastically impacted user needs in financial services. We devised a strategy to recruit participants from four generations.

Focus Groups by Generation

Market Research

To gain context and further explore our research goals, we investigated reports, articles, blogs, and customer reviews. I identified several opportunities for our client as well as a few topics of interest for our focus group discussions.

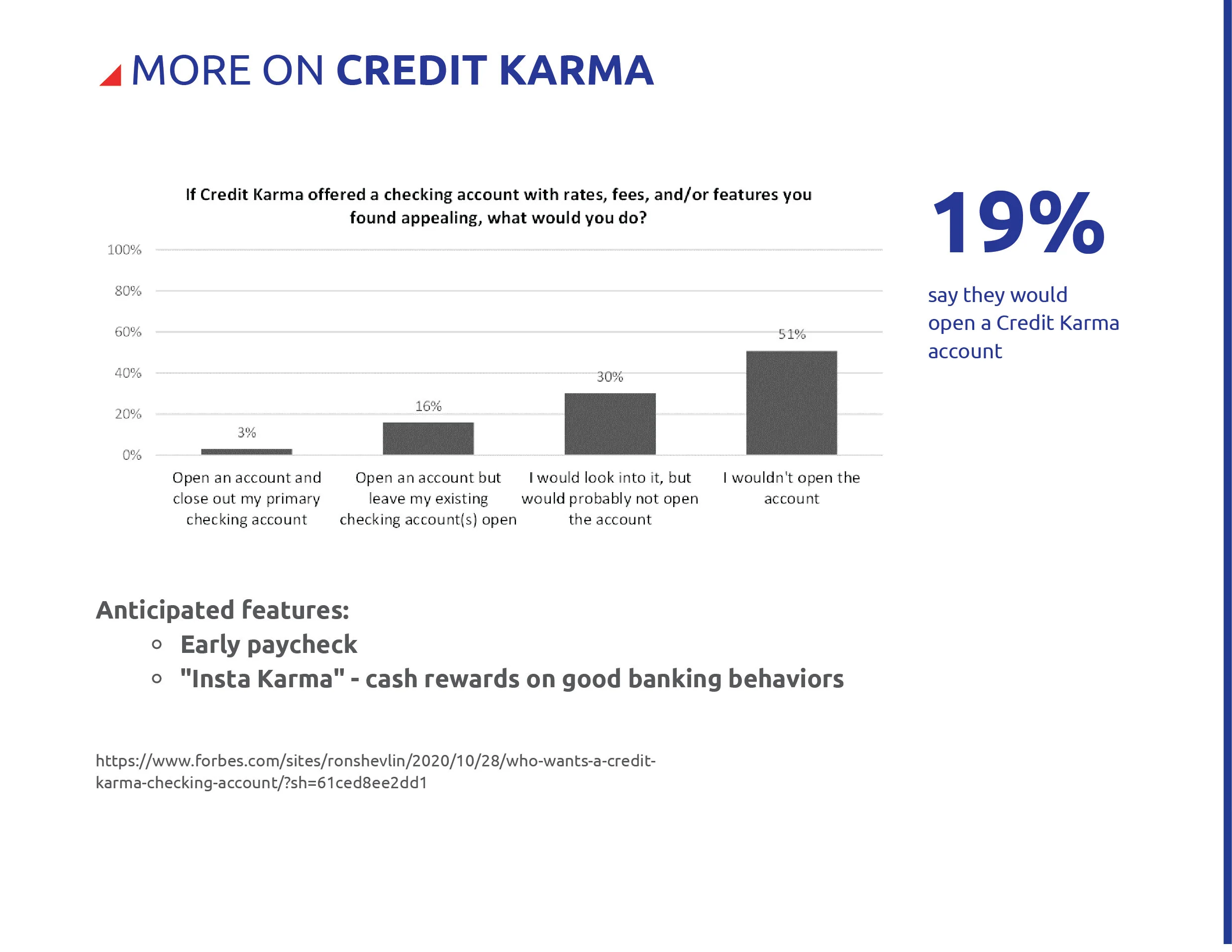

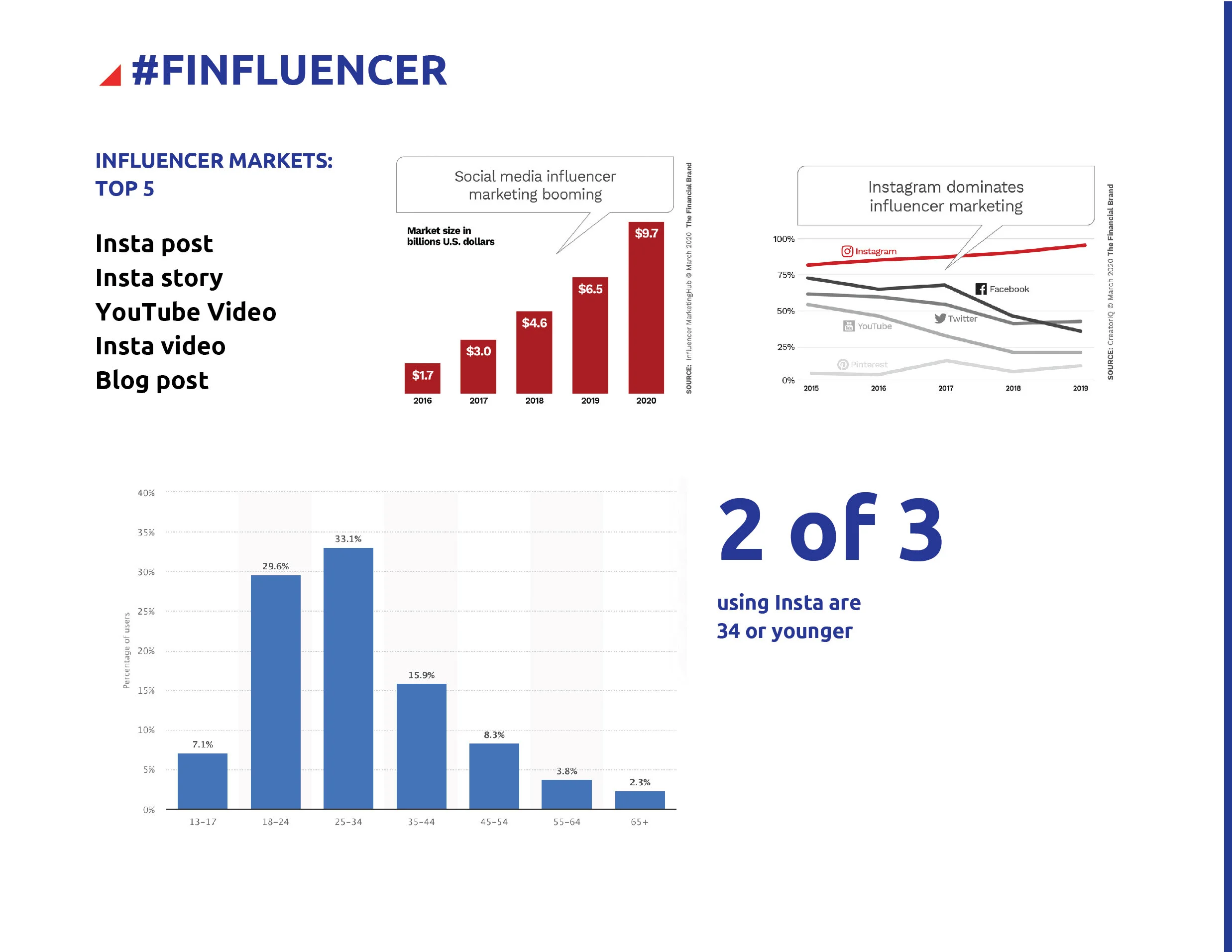

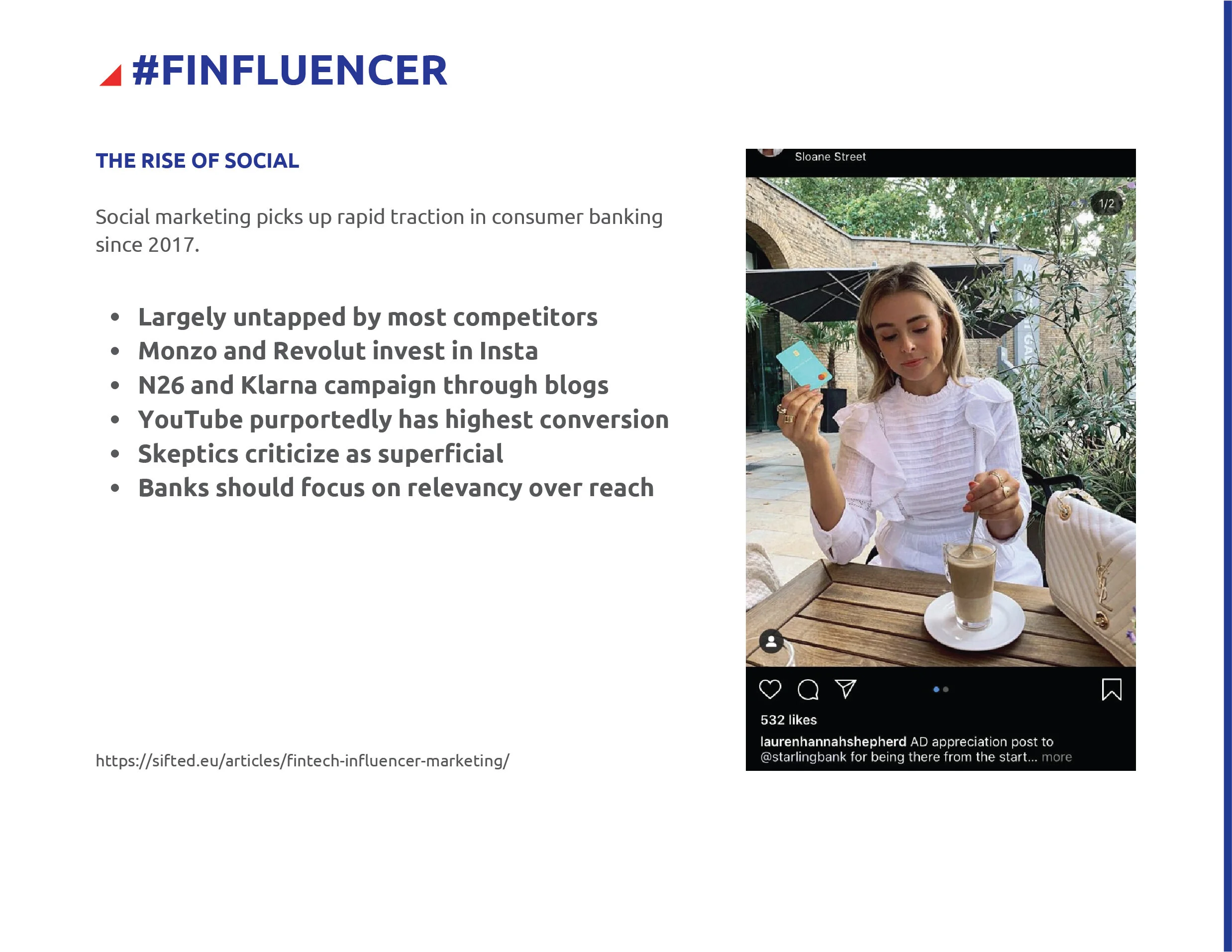

Excerpts from my market research report: Finfluencers were of great interest to the client’s marketing team.

Survey/Screeners

Along with demographics, our screener/survey evaluated and filtered participants by a range these criteria to acquire participants with a variety of backgrounds :

Preferred banking method (branch, desktop, mobile, etc.)

Importance of rewards

Importance of branch

Credit union / bank membership

Preferred banking relationships (digital bank, local bank, national bank, etc.)

Tenure with bank

Recent account openings

Types of financial products owned/used

Life events they are experiencing with large financial impact

Our participants were a diverse pool that varied in age, gender, income, education, and occupation.

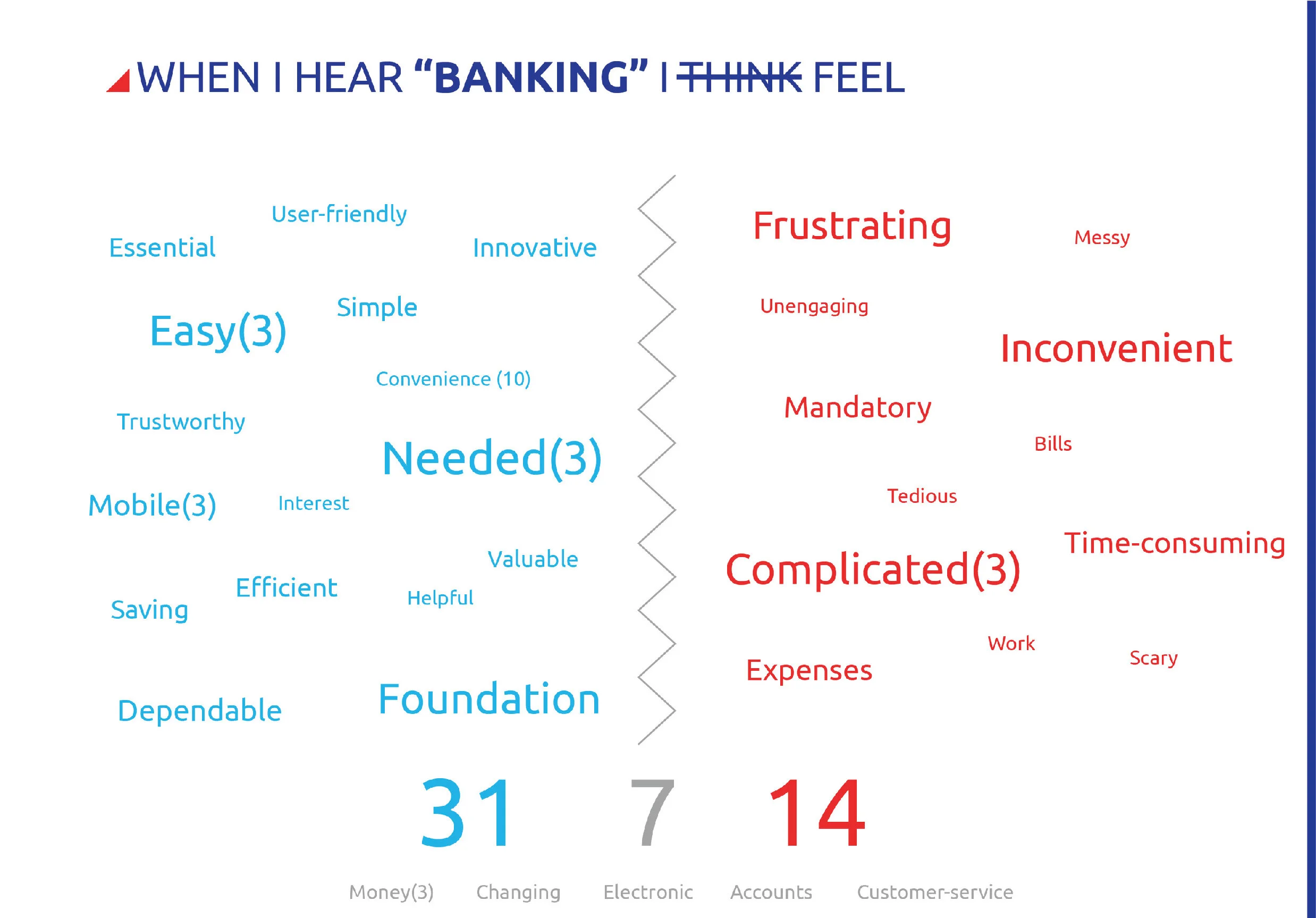

Focus Groups

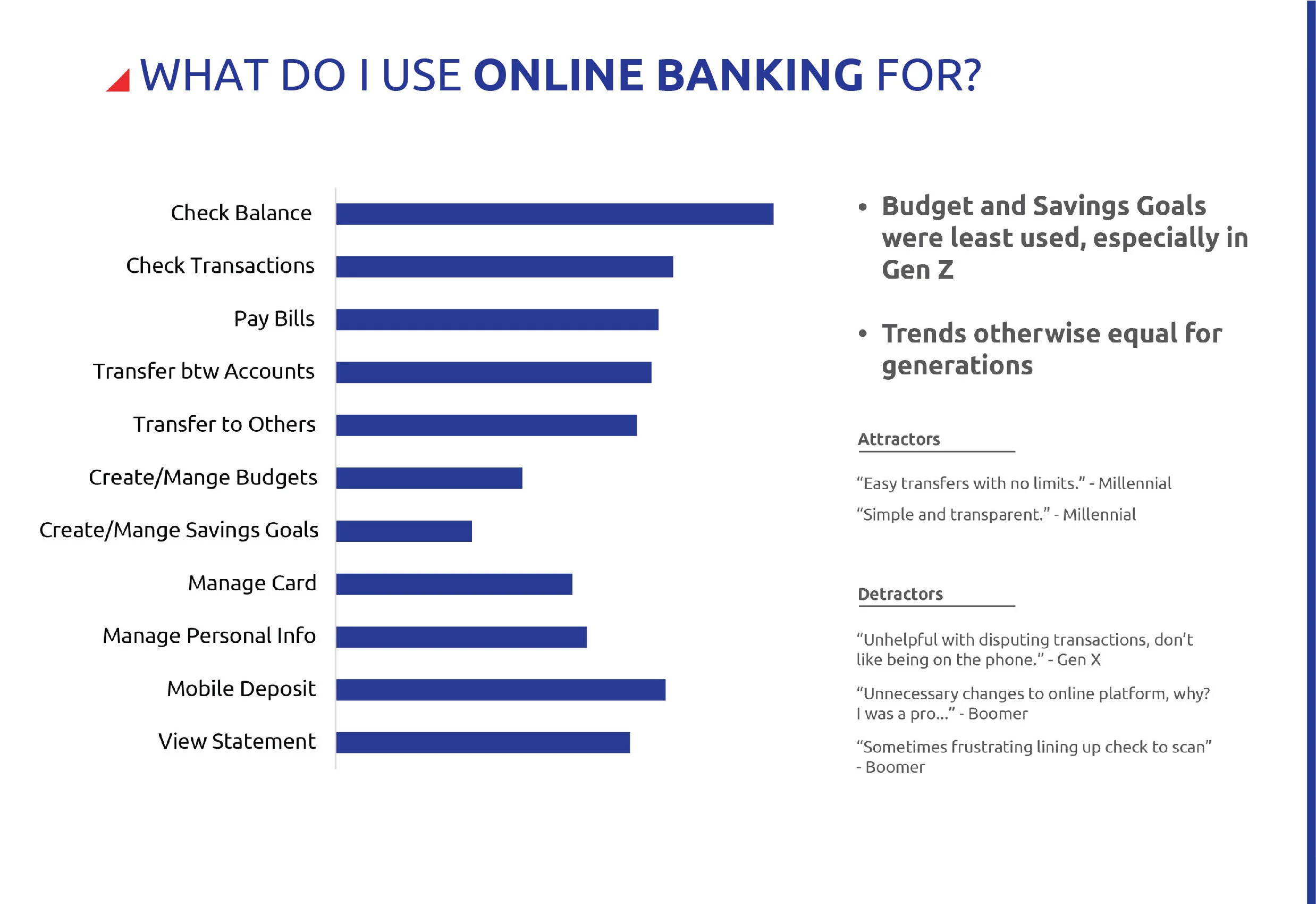

Due to the restrictions of COVID-19 we facilitated all of our focus group remotely using GoTo Meetings and recording each session in Lookback. We planned to conduct two rounds; the first round would feature the bank’s initial product concept, while the second round would feature a revision of the original concept. Each session was about an hour long with 6 to 8 participants. Tracey moderated while I flagged the metrics and recorded salient content.

First Round

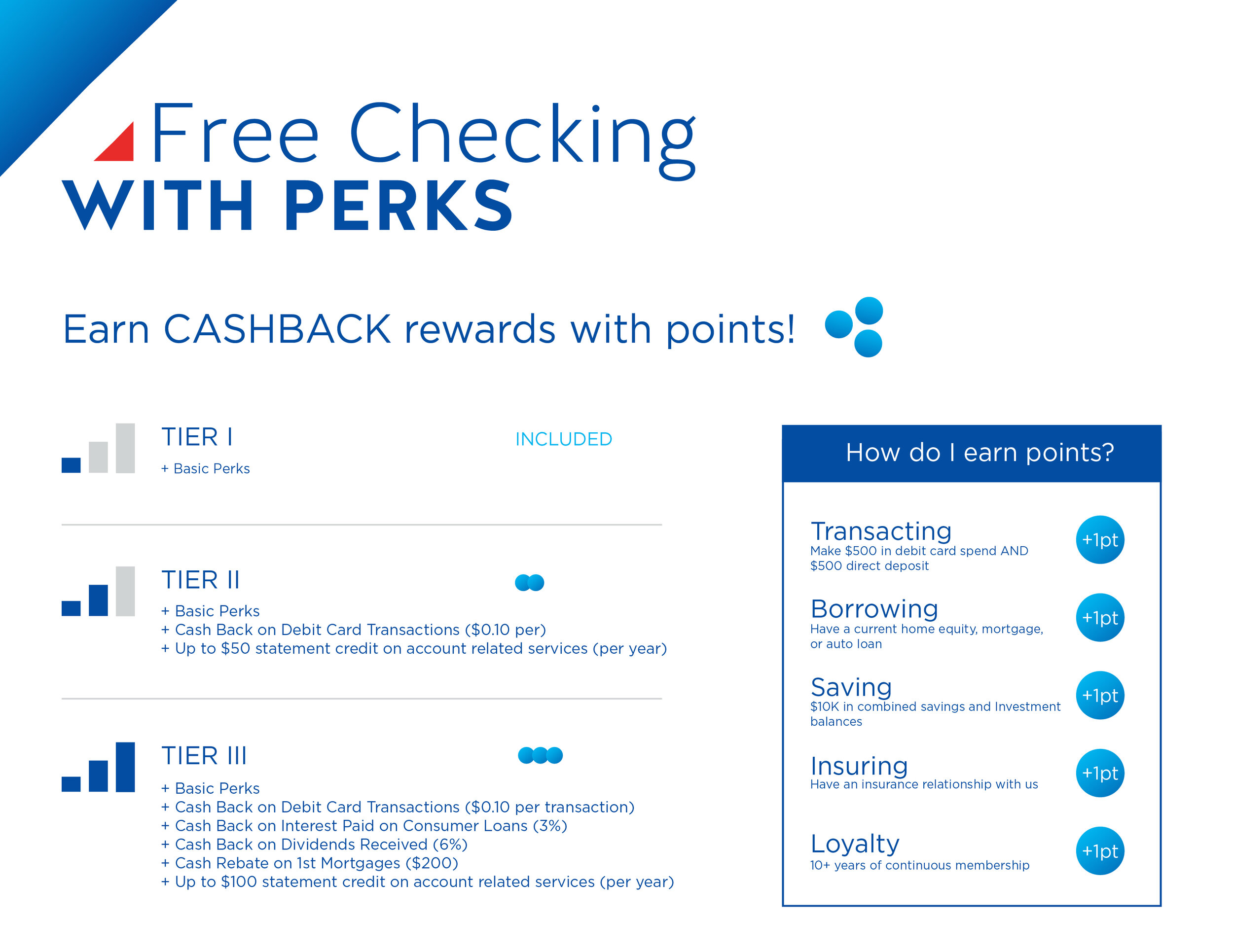

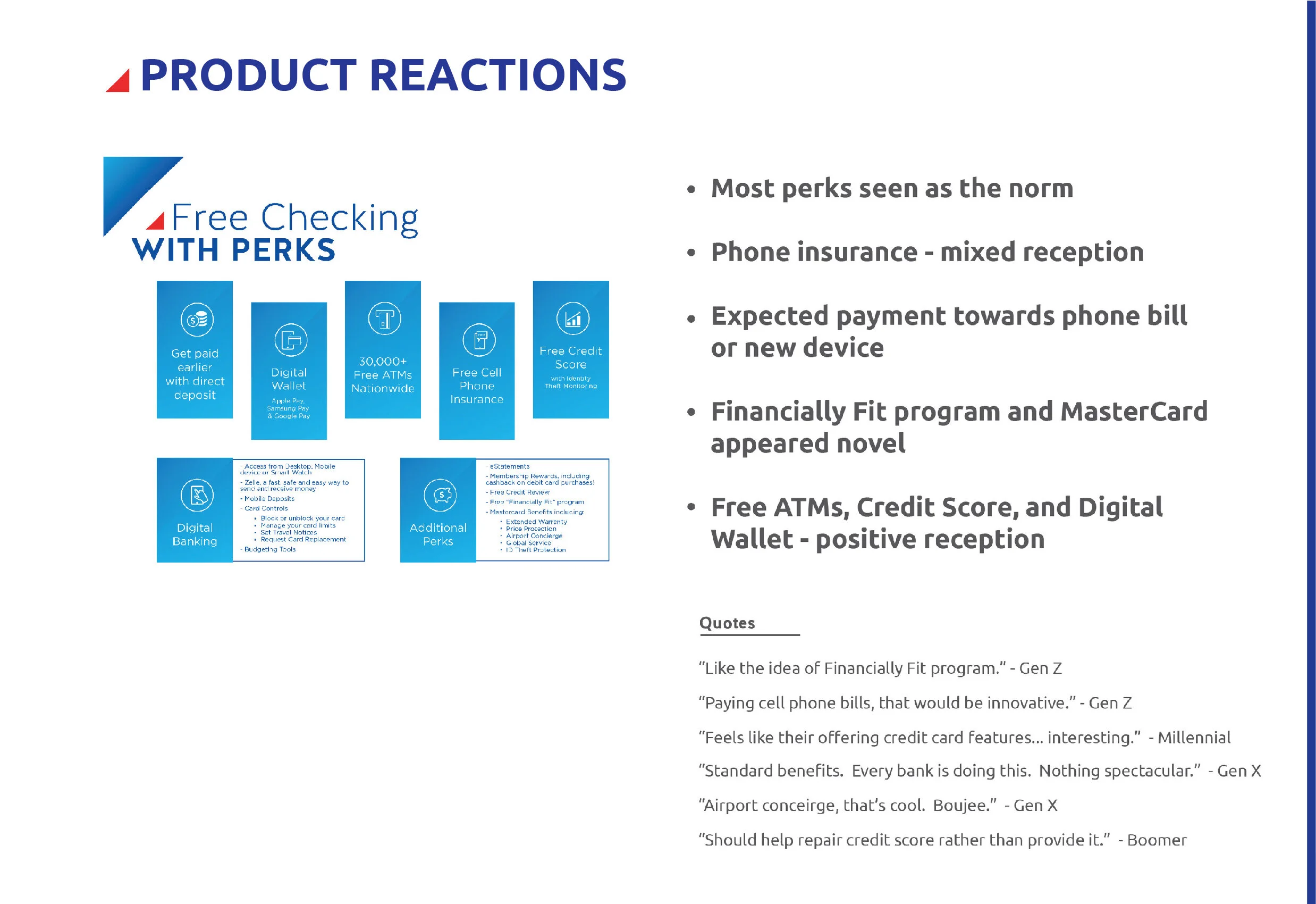

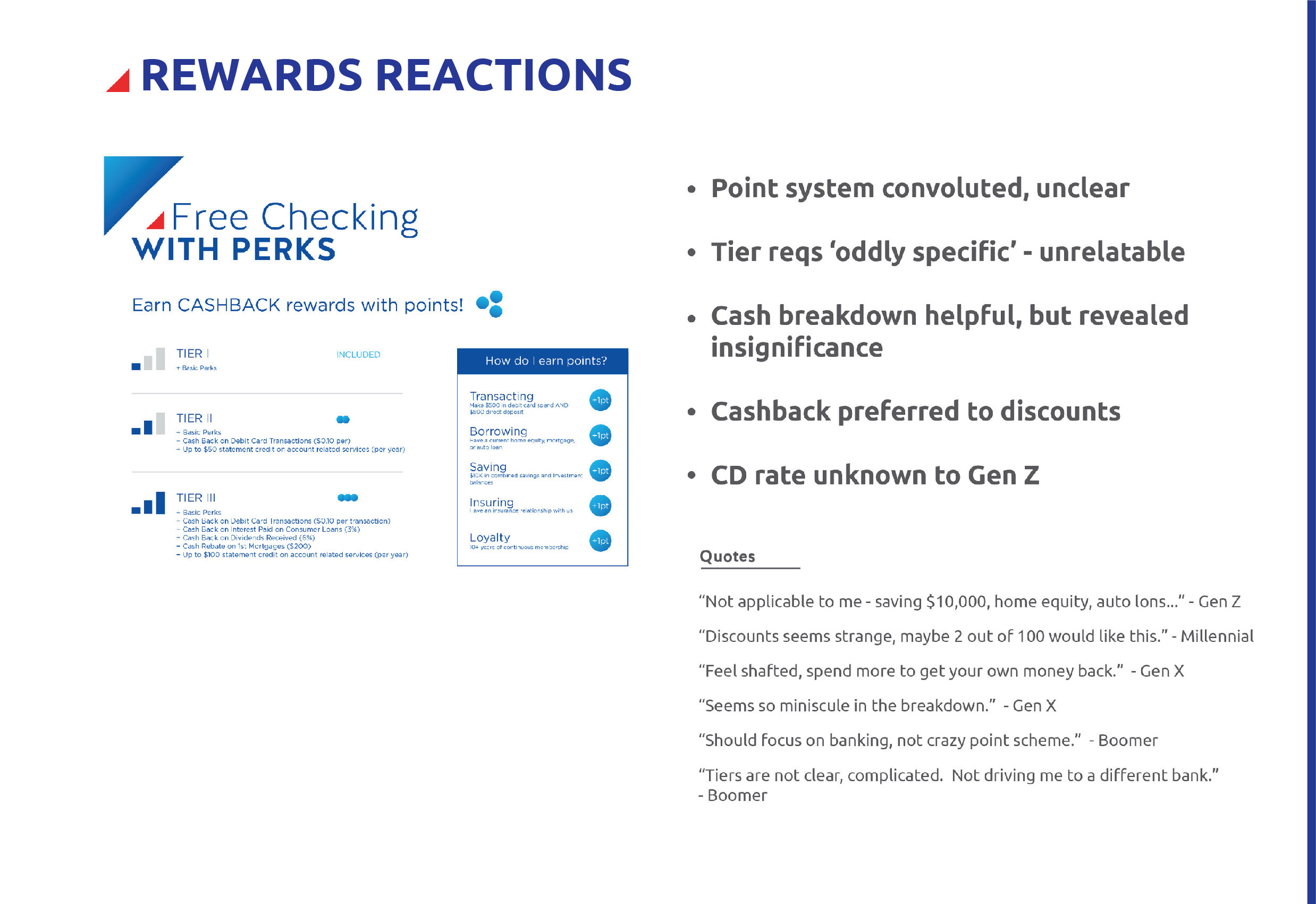

The credit union’s marketing strategy behind it’s cashback rewards accounts was to appeal to consumers with numerous banking “perks”, the primary of which was cashback. They planned to finance and monetize the rewards system by tiering the cashback with other products and incentives. While entry into Tier I was included with opening an account, account owners would need to qualify for at least Tier II to start collecting cashback. Tiers were then defined by a point system which tied to products and loyalty. If an account owner kept a certain amount of money in their savings account, or had enough tenure , or have an insurance membership, etc. they would earn a point.

In other words, the credit union’s system seemed a bit complicated and needed some visual aids! I created some presentation brochures that outlined the perks as well as the cashback rewards system. The bank was also curious how people felt “cashback” compared to “discounts” and so I created one other product variation too.

The client wanted to position it’s digital channels as “perks” to consumers.

Consumers were only eligible for certain benefits if they qualified by having enough points.

Second Round

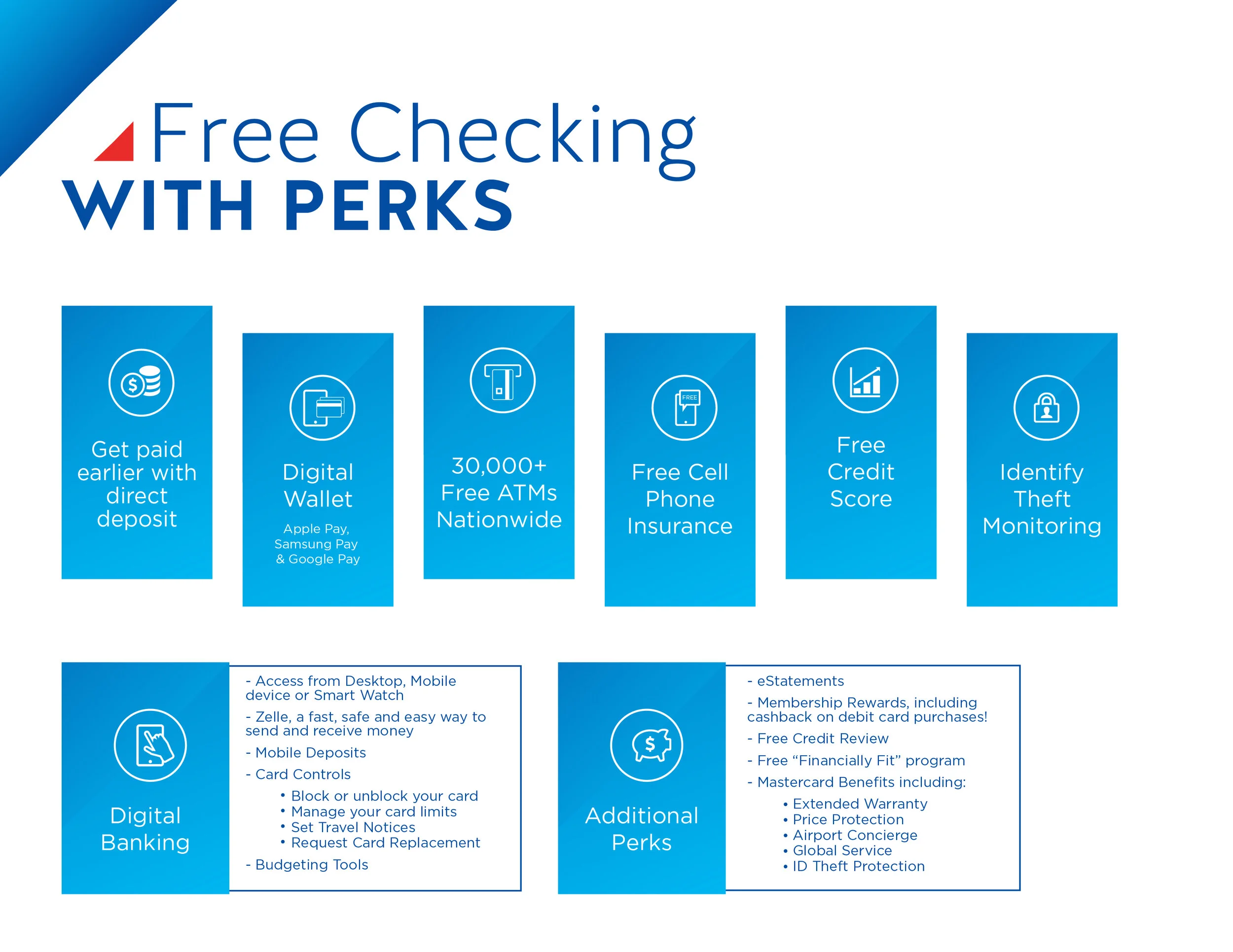

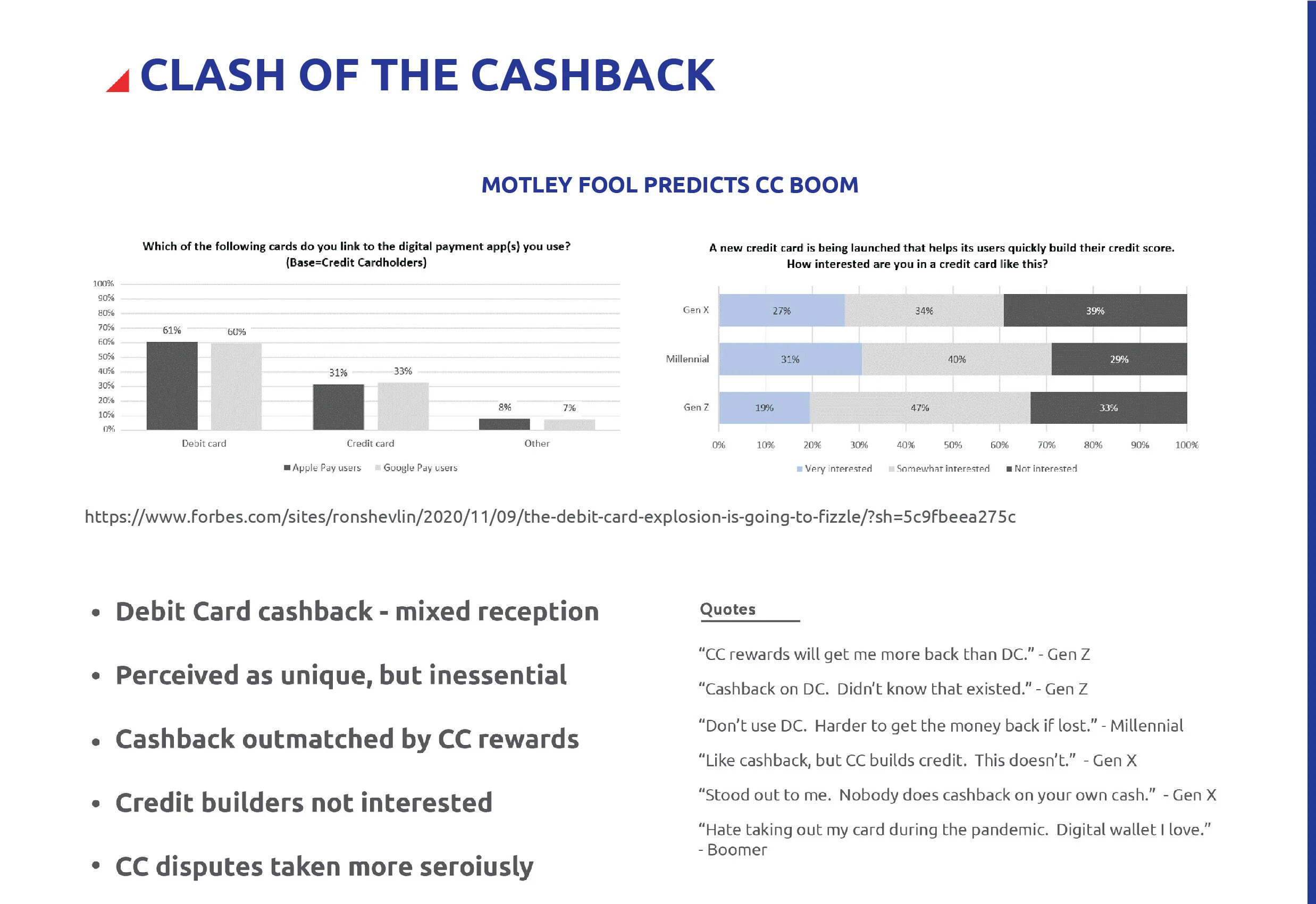

The focus groups reacted positively to the bank’s perks; however, many of the perks were perceived as either typical or superfluous although we found a few perks that piqued participants’ interests (discussed in detail later). One perk that both confused and interested participants was the advertisement of “Free Cell Phone Insurance.”

The participants confirmed my earlier intuition, the tiered cashback system appeared convoluted and obscure to participants. The true value of the system was questioned and several commented that it seemed disingenuous.

For the next round, I adjusted some of the perks and made a copy change to Free Cell Phone Insurance to add clarity. To combat participant’s anxiety with the cashback system, I created a brochure delivering the system with more transparency. I calculated what the average a person would earn in a year if they qualified as a Tier III account owner and made use of all of the perks.

We added a perk of Identity Theft Monitoring as the subject of security had been a hot topic in the last round.

Since the tiered-point system seemed shady, I created a more direct breakdown of consumer savings.

Findings

I called attention to several trends in financial behavior that revealed underlying consumer preferences and the performance of the product. The perks element of the product was well-received. I highlighted to the client which particular perks were superior, mundane, or confusing. As for the cashback rewards, I found that the cashback itself allured participants; but as part of tiered-point-system it also confused, frustrated, and angered them. I recommended other financial opportunities or incentives the credit union might consider instead as well as some revisions it might make to its perks.

Excerpts from my final report: includes survey stats, participant quotes/impressions, and product recommendations.

Conclusion

Although the client was disappointed that the tiered cashback system didn’t entice participants, they were extremely pleased with our report and surprised by many of our findings.

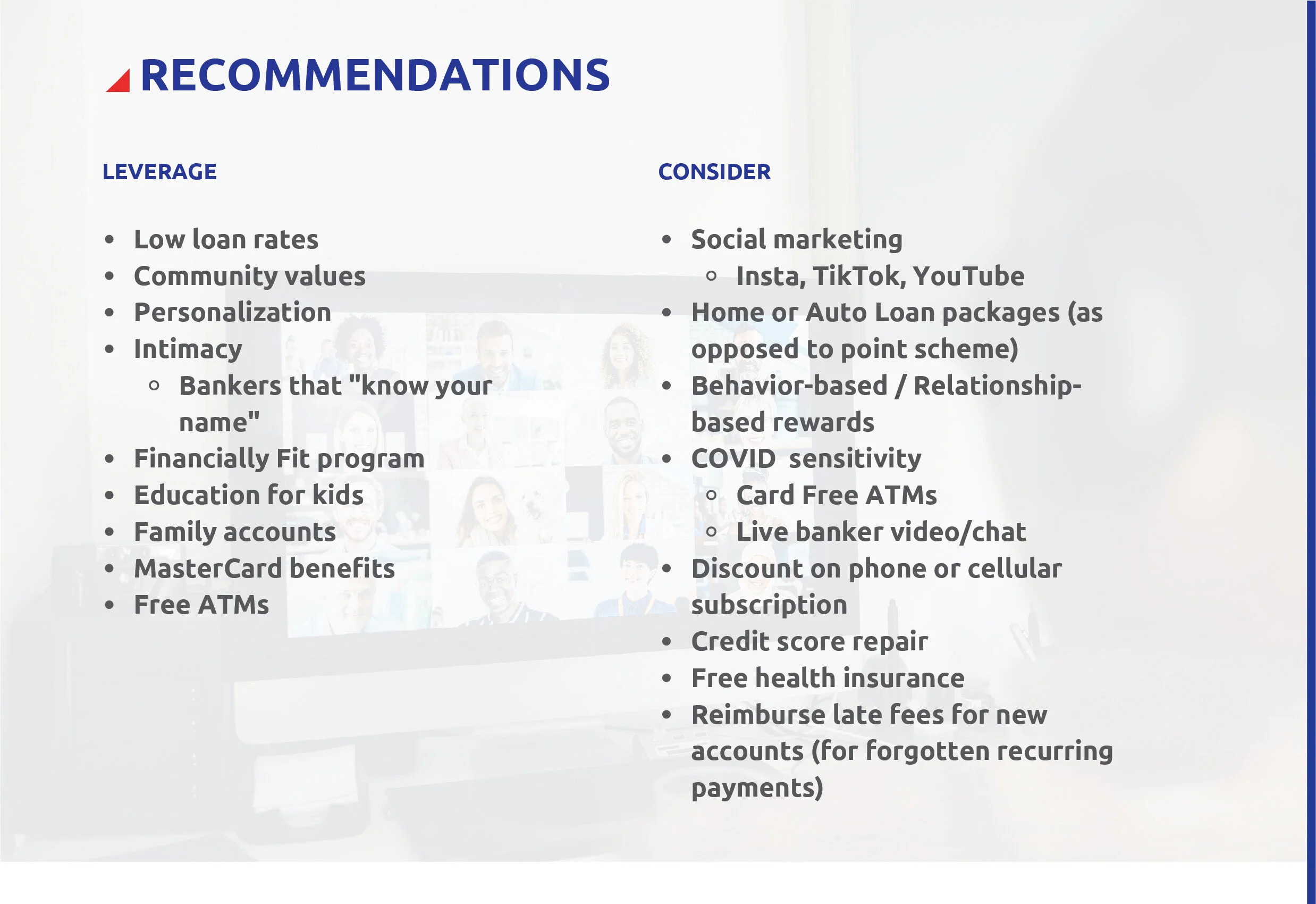

I offered several alternative options to the rewards system. One was to approach marketing from a perspective that was more meaningful to the consumer. For example, if the consumer needed to own product x, y, and z to get 300 dollars in rewards, then pitch the system as a “bundle” and keep the point-calculations on the back-end.

Since many of the perks were perceived as uninspired, I suggested the client play-up it’s strengths as a credit union. We identified several advantages in surveys and focus group: hospitality, education, teller’s that know my name, etc.

A “financial package” would be more meaningful to a consumer than an abstruse point system.

Consumers have become desensitized to online banking benefits, the credit union should play up consumer intimacy instead.

Lessons Learned

Build awareness through market research: this developed context for us and discovered opportunities for our client

The product might be wrong: the client appreciated our honest findings and constructive recommendations

See the client’s problem space, not just the problem: the broader objective was to inform the credit union’s creation of an enticing product, not just assess cashback rewards - we structured our study accordingly and the client was impressed with our strategy